![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

11 Cards in this Set

- Front

- Back

|

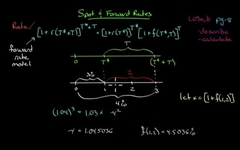

Spot yield curve X and y Discount factor Discount function |

Graph of rate against period Today's rate if 1dollar to be received in different period ( 6 months, or 1 year and so on. ) Discount factor and spot rate mapping for different period

|

|

|

Forward curve 3 yr loan starting at t2 F for price ( calculate by discount factor), f for rate |

Rate. .. r ( t,1) against period , If spot curve is upward sloping then forward curve will be upward sloping Cube root of (1+r2)(1+r3)(1+r4) |

|

|

If forward rate given spot rate |

Eg: 3 √ r3,1;, r4,1,;5,1 |

|

|

Forward rate model |

|

|

|

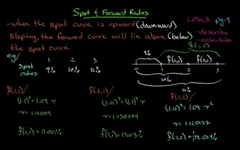

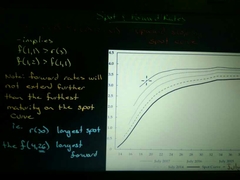

Relation btw spot curve and forward rate curve |

|

|

|

Find spot if series of fwd rate given |

Spot price is a geometric mean |

|

|

Yield to maturity against spot rates |

Weighted avg |

|

|

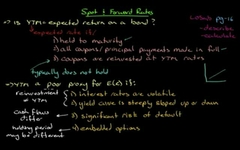

Ytm is expected return? |

|

|

|

Expected return is not ytm, it's calculation is annualised hpr Hpr Annualised hpr |

End - original/ original. Fv- PV/PV (1+hpr) power nth root of no of years ie 1/t. |

|

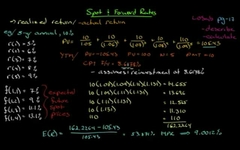

f(1,1) > r(2) f(1,2) > f(1,1) ,In eg it's year fwd If r(30) then max fwd is f(4,26) Why yield and price are inverse in relationship ?? |

|

|

|

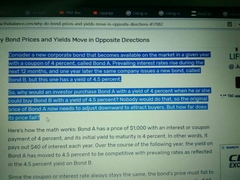

riding the yield curve |

Wider the spread , longer the bond, greater the total return. |