![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

77 Cards in this Set

- Front

- Back

|

Delta Hedging 3 components in Overnight Profit |

1. Gain on stocks 2. Gain on options 3. Interest on borrowed/lent money |

|

|

Delta Hedging Breakeven |

The price movement with no gain or loss to delta-hedger is: +/- Sσ√h

|

|

|

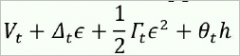

Delta-Gamma-Theta Approximation V t+h = |

These are the Greeks controlling profits.

|

|

|

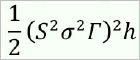

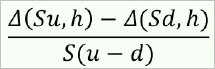

Boyle-Emanuel Formula Periodic variance of return when rehedging every h in period i: Var[R h,i] = |

|

|

|

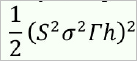

Boyle-Emanuel Formula Annual variance of return when rehedging every h in period i: Var[R h,i] = |

|

|

|

Greeks for Binomial Trees Δ(S,0) = |

|

|

|

Greeks for Binomial Trees Γ(S,0) ~= Γ(S,h) = |

|

|

|

Greeks for Binomial Trees θ(S,0) = |

|

|

|

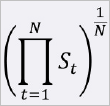

Exotic Options - Asian Option S bar = |

A(S) arithmetic average G(S) geometric average |

|

|

Exotic Options - Asian Option A(S) = |

|

|

|

Exotic Options - Asian Option G(S) = |

|

|

|

Exotic Options- Asian Option G(S) ? A(S) |

G(S) <= A(S) |

|

|

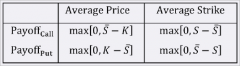

Exotic Options- Asian Option Summary table for Average Price & Average Strike with Call & Put Payoffs |

|

|

|

Exotic Options Asian Option ? otherwise equivalent ordinary option |

<= The value of an Asian option is less than or equal to the value of an otherwise equivalent ordinary option. |

|

|

Exotic Options - Asian Option As N (period) increases: -Value of average price option ... -Value of average strike option ... |

As N increases: -Value of average price option decreases. -Value of average strike option increases. |

|

|

Exotic Options - Barrier Option 3 types: |

1. Knock-in 2. Knock-out 3. Rebate |

|

|

Exotic Options - Barrier Option Knock-in |

Goes into existence if barrier is reached. |

|

|

Exotic Options - Barrier Option Knock-out |

Goes out of existence if barrier is reached. |

|

|

Exotic Options - Barrier Option Rebate |

Pays fixed amount if barrier is reached. |

|

|

Exotic Options - Barrier Option Down vs. Up |

If S0 If S0>B: Down-and-in, down-and-out, down rebate |

|

|

Exotic Options - Barrier Option Ordinary option = |

Knock-in + Knock-out = Ordinary Option |

|

|

Exotic Options - Barrier Option Barrier option ? Ordinary option |

Barrier option <= Ordinary option |

|

|

Exotic Options - Barrier Option Special relationships: -If barrier <= K: -If barrier >= K: |

-If barrier <= K: up-and-in call = ordinary call -If barrier >= K: down-and-in put = ordinary put |

|

|

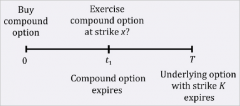

Exotic Options - Compound Option Timeline |

|

|

|

Exotic Options - Compound Option The value of the underlying option at time t1 = |

|

|

|

Exotic Options - Compound Option The value of the compound call at time t1 = |

|

|

|

Exotic Options - Compound Option The value of the compound put at time t1 = |

|

|

|

Exotic Options - Put-call parity for Compound Option: CallonCall - PutonCall = CallonPut - PutonPut = |

|

|

|

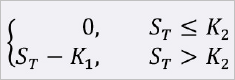

Exotic Options - Gap Options K1: |

Strike Price. determines the amount of the payoff. |

|

|

Exotic Options - Gap Options K2: |

Trigger Price. determines whether the option will have a payoff.

|

|

|

Exotic Options - Gap Options Payoff for Gap Call = |

|

|

|

Exotic Options - Gap Options Payoff for Gap Put = |

|

|

|

Exotic Options - Gap Options GapCall = |

where d1 and d2 are based on K2 |

|

|

Exotic Options - Gap Options GapPut |

where d1 and d2 are based on K2 |

|

|

Exotic Options - Gap Options GapCall - Gap Put = |

|

|

|

Exotic Options - Exchange Option C(A receive,B give up) = |

|

|

|

Exotic Options - Exchange Option P(A give up,B receive ) = |

|

|

|

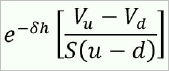

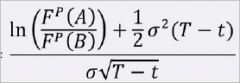

Exotic Options - Exchange Option d1 = |

|

|

|

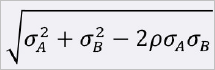

Exotic Options - Exchange Option σ = |

|

|

|

Exotic Options - Exchange Option C(A,B) = P(?,?) |

C(A,B) = P(B,A) |

|

|

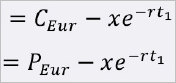

Exotic Options - Exchange Option C(A,B) - P(B,A) = |

F^P (A) - F^P (B) |

|

|

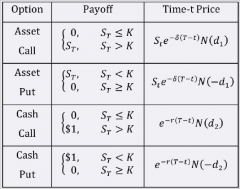

Exotic Options - All or nothing Options Summary Table |

|

|

|

max(A,B) = ... = ... |

= max(0,B-A) + A = max(A-B,0) + B |

|

|

max(cA,cB) = ... c>0 max(cA,cB) = ... c<0 |

= c*max(A,B) c>0 = c*min(A,B) c<0 |

|

|

max(A,B) + min(A,B) = --> min(A,B) = |

= A + B = -max(A,B) + A + B |

|

|

Exotic Options - Forward Start Option For a call option expiring at time T whose strike is set on future date t to be XSt: |

C(St,XSt,T-t) prepaid forward on an option. Strike price will be a multiple of St. |

|

|

Exotic Options - Forward Start Option C(St,XSt,T-t) = ... = ... |

|

|

|

Exotic Options - Forward Start Option For C(St,XSt,T-t), d1 = |

|

|

|

Exotic Options - Forward Start Option The time-0 value of the forward start option is: V0 = |

|

|

|

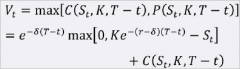

Exotic Options - Chooser Option For an option that allows the owner to choose at time t whether the option will become a European call or put with strike K expiring at time T: Vt = |

|

|

|

Exotic Options - Chooser Option V0 = |

|

|

|

Volatility σ- bet on volatility is a ... |

calendar spread. |

|

|

Volatility σis not directly ... |

observable. |

|

|

Stochastic Volatility σ |

Volatility can vary by time & other factors. However, the BS framework assumes that σdoes not depend on St, Xt, or t. In other words, σ is constant. |

|

|

2 methods for estimating σ |

1. Implied σ: start with option prices & a pricing model & back outσ from option prices. 2. Historical volatility: start with historical stock prices & calculate the st. dev. of the logged changes in price over short periods of time. |

|

|

Implied σ importance: |

*Allows pricing other options on the same stock *Quick way to describe option prices *σ skew is a measure for how good BS is -Implied σ tends to decline as period to expiry increased &σdeclines as K increases. |

|

|

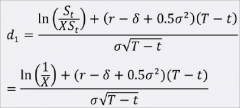

Implied σ when d2 = -d1 can be on the exam. Otherwise not on exam, since back out is iterative. |

The prepaid forward prices of stock & strike are equal. |

|

|

Annual Historical Variance of Total Returns |

*Sample mean is not subtracted from each ε. *Mean is assumed to be zero since h is assumed to be small. *Look for direction from exam question whether to subtract *Multiply by the # of trading days in a year to annualize the variance (252) |

|

|

Overnight profit on a delta-hedged portfolio |

1. The change in the value of the option. 2. Δ * change in the price of the stock. 3. Interest on the borrowed money. |

|

|

Market Maker Profit = (in words) |

- (Change in stock price + time decay + interest effect - dividend effect) |

|

|

Exotic Options - Asian Option Pays based on ... |

Average not final |

|

|

Average Strike Option |

There is no strike price. Payoff is based on final price and the avg price. |

|

|

Quotients of stock prices over non overlapping intervals are independent. |

TRUE

|

|

|

Exotic Options - Compound Option Definition |

Option whose underlying asset is another option which expires later. |

|

|

Ex-dividend |

After div is paid. |

|

|

Cum-dividend |

Including the div; before div is paid |

|

|

Exotic Options - Compound Option Not exercising the Ameri option corresponds to ... |

to exercising both parts of the compound option. |

|

|

Exotic Options - Compound Option Exercising the Ameri option early corresponds to ... |

to not exercising the compound option. |

|

|

Exotic Options - Compound Option Exercising the Ameri option at maturity corresponds to ... |

to exercising only the first part of the compound option. |

|

|

Expectation proportion of a rv over a range is ... |

the partial expectation conditional on that range divided by the total expectation.

Partial expectation = Total Exp * Exp Proportion |

|

|

Exotic Options - All or nothing Options Delta |

Cancellation does NOT occur for all or nothing options, so the delta formula is more complicated. |

|

|

Exotic Options - Cash or nothing Options C = |

= delta S - CONC() |

|

|

Exotic Options - Gap & All or nothing Options Delta hedging is not so effective for options because ... |

the payoff is discontinuous. |

|

|

Exotic Options - Gap Options Define |

Option with a trigger & a strike price where the two are unequal. Election is not optional and payoff may be negative. Worth less than ordinary option. |

|

|

Exotic Options - Gap Options Delta may be ... |

Delta may be > 1 for a gap option. |

|

|

Out-performance Option Define |

Since it pays off only if the option asset out performs the asset it's being exchanged for S: price of asset to be received Q: price of asset to be exchanged |

|

|

Out-performance Option Volatility depends on ... |

on both assets. |