![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

32 Cards in this Set

- Front

- Back

|

IAS 1 only explains how to present financial statements |

- Recognition, measurement & disclosure are explained in the remaining IFRS |

|

|

With Presentation in mind IAS1 sets out the |

- Objectives of IAS 1 - general features of Financial statements |

|

|

Comparability appears in: |

-IAS 1 as the ultimate objective for setting out the presentation requirements and guidelines |

|

|

General purpose financial statements are defined as those intended to |

- Meet the needs of users - Who are not in a position to prepare reports tailored to their particular information needs. |

|

|

5 Main statements in a complete set of financials |

1. Statement of Financial position (SOFP) 2. Statement of comprehensive Income (SOCI) 3. Statement of Changes in Equity (SOCE) 4. Statement of Cash Flow (SOCF) 5. Notes to the Financial Statements (Notes) |

|

|

8 General Features |

1. Fair Presentation & compliance with IFRS 2. Going Concern 3. Accrual Basis 4. Materiality & aggregation 5. Offsetting 6. Frequency of reporting 7. Comparative information 8. Consistency of presentation |

|

|

Fair presentation is generally achieved by: |

Application of the IFRSs with extra disclosure if needed |

|

|

Fair Presentation Needs: |

Compliance with IFRSs and extra disclosure where needed, but it alos needs * Application of the CF's definitions and recognition criteria * Faithful representation (complete, neutral and free from error) * Reliability, relevance, comparability & understandability |

|

|

Fair presentation IAS1 needs |

1 Fundamental Qualitive Characteristics (QC): faithful representation & 3 enhancing QC's: relevance, comparability & understandability |

|

|

Departure from the IFRS |

If compliance will be so misleading that it conflicts with the objective of financial reporting. - Depart from the IFRS unless the relevant regulatory prohibits departure. If you depart, extra disclosure will be needed to explain the departure. If you do not depart, extra disclosure will be needed to explain why you felt you should depart and the adjustments you would have liked to have made but didn't |

|

|

Going Concern (GC) |

* The entity is a going concern * The entity is not a going concern * There is significant doubt as to whether the entity will be able to continue as a going concern or not |

|

|

The Accrual Bassis |

Is used for all statements makingg up he set of financial statements with the exception of the statement of cash flows, which uses teh cash basis. |

|

|

To summarise information, |

is to combine (aggregate ) items that we beleive are not material enough to show seperately |

|

|

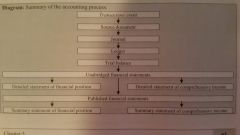

Summary of the Accounting process |

|

|

|

Items are material |

If the decision of teh users could be infuenced if they were mistated or omitted, individually / collectively. Materiality depends on the size/ nature / both |

|

|

Minimum Comparative Info: |

We must show prior year information (for numerical and narrative information) Prior year info for narrative info is only needed if relevant. Comparisons may be needed in reverse |

|

|

Voluntary Comparative information |

- extra comparative years can be given if we wish - We can give extra comparatives for just 1 statement if we wish but the notes supporting this statement must include all previous periods - All previous periods must comply with IFRS |

|

|

Compulsary comparitive information |

-An extra comparative year must be given if a materal retrospective adjustment is made. - This extra comparative year refers to opening balances of the prior period - This extra comparative year: |

|

|

Consistency Refers to |

Presentation / classification of teh items being the same from one period to the next. It is essential for comparability. Thus if presentation or classification must change it is accounted for in reclassification. |

|

|

Current and Non Current |

We can seperate assets and liabilities into current and non current or list them in order of liquidity instead (if this is reliable & more relevant. |

|

|

Non curret assets are those: |

That are not current assets |

|

|

Current assets are those: |

- We expect to realise within a year of the reporting date - We hold mainly to trade - We expect to use/ realise / sell within operating cycle or - That are cash / cash equivalents (uness restricted |

|

|

A Non current Liability is one: |

That is not current |

|

|

A Current Liability are those: |

- We expect to settle within year of teh reporting date - We hold mainly to trade - We expect to settle within the operating cycle or - We do not have an unconditional right to delay settlement beyond one year from reporting date |

|

|

Minimum Disclosure on the SOFP face |

IAS1.54 lists line items that must always appear on the face of the SOFP Extra disclosure on the SOFP face: IAS 1. 55 Judgement is needed to decide if further line items, headings and totals are relevant to users understanding |

|

|

More SOFP related disclosure: |

Extra sub classification may be needed, which could be onteh face or in the notes. These depend on - Materiality, liquidity, nature & function of the assets and - materiality, timing & nature of liabilities |

|

|

Consolidated SOCI |

If the SOCI relates to a consolidated group thta includes a partly owned subsidary, the SOCI must show how the Consolidated TCI will be allocated between the parents owners and the non controlling interests |

|

|

The SOCIE must present |

Changes in equity thus it needs reconciliations from each component of equity. - each class of contributed equity - retained earnings (P/L) - each of the 6 items of OCI |

|

|

The SOCIE may also preset |

The amount of recognised dividend distributions and dividends by share (DPS) The dividend amount and DPS may be shown in teh notes instead Not all dividends are recognised |

|

|

Retrospective Adj's are: |

Presented in the SOCIE not changes in equity. Presentation of RA's must include: - The effect on each item of equity for each prior period and the opening current period balances. |

|

|

Structure and content of the five financial statements |

- Minimum disclosure requirements (both on the face of ecah component and in teh notes) Current (C) vs Non current (NCL) Effect of refinancing of liability and breach of covenants liabilities (CL or NCL) - SOCI How to present expenses (functions / nature method) How to present the P/L How to present OCI (& reclassification adjustments) How to present TCI (and if it is a consolidated group how to allocate this between the owners and the Non controlling interest -SOCIE How to present each component of equity How to present within these component transactions with owners How to present the effects of changes in accounting policy and correction of errors - SOCF How to separate cash flows into operating, investing and financing activities - Notes Compliance with IFRS Basis of preparation and significant accounting policies Measurement bases Sources of estimated uncertainty How the entity manages its capital Items included in the other 4 statements that need supporting detail to be disclosed Items not included in the other 4 statements that do require disclosure

|

|

|

The Financial Report = Financial statements + Other statements and reports |

Financial statements must comply with IFRS - Statement of financial position *Gives info about the financial position * presents assets, liabilities & equity - Statement of changes in Equity * Gives info about changes in financial position Parents movement in equity - Statement of Comprehensive Income * Gives info on financial performance * Parents income and expenses = TCI where TCI is split between P/L & OCI - Statement of Cash Flows * Gives info about cash generating ability * presents cash movements analysed into operating, investing and financing activities - Notes to the Financial Statements * Gives info about line items that are in the other statements but also items that have not been recognised in the other statements but may still be relevant info for the users |