![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

87 Cards in this Set

- Front

- Back

|

1933 Act Regulates |

Original Issuances of Securities |

|

|

1934 Act Regulates |

Purchases and Sales after Initial Issuance |

|

|

If the Investor is Passive |

i.e. Relies solely on the management of others to make money, the investment is most likely a security. |

|

|

Limited Partnership Interests |

are deemed securities. |

|

|

General partnership interests are |

NOT deemed to be investments. |

|

|

1933 Act is to Assure |

Investors have sufficient information to make informed investment decision. |

|

|

1933 Act Requires most Issuers |

to Register new issues of securities with the SEC and to provide Prospectus containing material information regarding the securities to prospective investors. |

|

|

The SEC does not |

Guarantee accuracy of prospectus, evaluate offering's financial merits or give assurances against loss. |

|

|

1933 Act Registration Requirements only apply to |

Issuers, Underwriters, Dealers |

|

|

An Underwriter is an |

Intermediary who sells an issuer's securities to the general public or to dealers. |

|

|

Most Securities cannot be sold unless |

they are first registered with the SEC. |

|

|

Registration Statement Consists of 2 parts |

Prospectus. Detailed Info regarding securities. |

|

|

The Prospectus is a |

Written offer to Sell Securities. |

|

|

The Prospectus Summarizes |

important information contained in the Detailed Information regarding securities. |

|

|

Each Investor must receive a copy of the |

Prospectus before or Contemporaneous with every sale of the security. |

|

|

Information about Securities Issued must include |

Audited balance sheet Dated not more than 90 days before filing and Profit and Loss for the past 5 years. Financials must be certified by a public accounting firm registered with the PCAOB. |

|

|

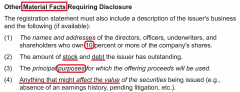

The Registration Statement must also include a description of the business and the following |

|

|

|

Shelf Registrations |

For Issuers constantly issuing new securities, issuers can prepare just one registration statement for all securities that they will offer in the future. |

|

|

Shelf Registration is permitted if the issuer has |

continuously filed under the 1934 Act for one year and the information is continuously updated. |

|

|

SEC Reviews the Registration Statement to ensure |

Both Parts are complete. |

|

|

The Registration Statement becomes effective on |

the 20th day after its filingwith the SEC unless issues a refusal or stop order. |

|

|

Blue sky laws |

State laws governing stock sales |

|

|

No sales is allowed within |

30 Days before Registration unless issuance is exempt. |

|

|

After Registration but before Effectiveness (Waiting Period), there is a |

20 day waiting period between registration and filing date. |

|

|

Some sales are allowed during after registration but before Effectiveness: |

Oral offers to sell but no written offers. Tombstone ads. Preliminary prospectus (red herring) can be made. Summary prospectus are allowed. |

|

|

Seasoned issuers are issuers that have been |

continuously reporting under the 1934 act for at least 12 months, have not failed to pay a dividend or required payment on preferred stock and have not defaulted on material debt or a long term rent obligation. |

|

|

Well-known Seasoned issuers |

are issuers with at least $700M in equity outstanding worldwide in the hands of persons not affiliated with the issuer or most issuers that have issued at least $1B in non convertible securities in the last 3 years. |

|

|

A Well-known Seasoned issuer |

may make Oral or Written offers at any time. |

|

|

WKSIs also have a special form of |

Shelf Registration that is effective immediately. |

|

|

Exemptions from 1933 Registration Act |

Securities Exemptions. Transaction Exemptions. |

|

|

The Following Securities never have to be Registered: |

BRNGS Securities issued by: Banks and S&Ls. Not for Profits. Governmental. Regulated Common Carriers (railroads). Short Term Commercial Paper with 9months or less Maturity Date. Insurance Policies. Charitable Organizations. |

|

|

Transaction Exemptions |

Casual Sales - Not by issuer, underwriter or dealer. Exchanges with Existing Holders and Corporate Reorganizations. Government approved exchanges that occur as a result of corporate reorganization. |

|

|

Intrastate Sales |

Section 3(a)(11) of the 1933 Act provides an exemption for securities offered and sold only to persons who are residents of the issuer's state. |

|

|

Under rule 147, which implements Section 3(a)(11), |

the entire issue must be offered and sold only to residents of that state, the issuer must do at least 80 % of its business in that state, and purchasers cannot resell the securities for 9 months to nonresidents of that state. |

|

|

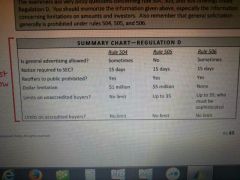

Private Offering Exemption - Regulation D |

Regulation D Exempts "private" offerings and the SEC has 3 private offering exemptions under Regulation D: 504, 505 and 506. |

|

|

Purchasers of Regulation D Securities may not |

Immediately re offer Securities to the public. Must hold for 2 years or more. "Restricted" stock. |

|

|

SEC must be notified of Regulation D stock within |

15 days of sale |

|

|

Rule 504 - $1M limit |

To be exempt under the 504, the issuance of securities may not exceed $1M within 12 months. |

|

|

Rule 504 has no limitations on |

Number or type of purchasers |

|

|

Rule 504 generally does not require any specific |

Disclosure to investors prior to sale. |

|

|

If Rule 504 is registered under state law, the general prohibition against |

General advertising does not apply |

|

|

To be exempt under Rule 505 |

The issuance of securities may not exceed $5M within 12 months |

|

|

Securities issued under Rule 505 may be sold to any number of |

Accredited investors and 35 or fewer unaccredited investors |

|

|

An accredited investor is |

A bank. Person with $1M net worth or $200K annual income. Officers or directors of the issuer |

|

|

If only accredited investors purchase Rule 505 stock |

No disclosure is required. If any unaccredited investors, all investors must be given annual audited financials. |

|

|

Under Rule 506 there is |

No limit to the amount of stock to be sold |

|

|

Rule 506 stock may be sold to any number of |

Accredited investors and 35 unaccredited but sophisticated investors |

|

|

Summary |

|

|

|

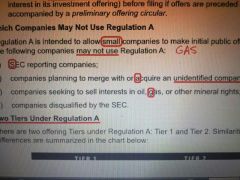

Regulation A Simplified filing |

Not a registration exemption but a simplified form of registration to allow small companies to make public offerings quickly and less cost. |

|

|

Companies using Regulation A file an |

Offering statement which consist of a Notification and an Offering Circular |

|

|

Companies may test the waters first before filing if |

Offers are preceded or accompanied by a Preliminary Offering Circular. |

|

|

Which companies may not use Regulation A: |

|

|

|

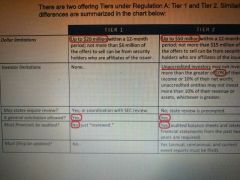

Tiers |

|

|

|

Section 11 imposes |

Civil liability for misstatements, intentional or not. |

|

|

Section 12 imposes |

Civil liability if required registration not made, if prospectus was not given, if materially false statements were made or omitted in connection with sales or offers to sell. |

|

|

Section 17 imposes |

Criminal penalties against fraud. Enforced by SEC and prosecuted by justice department |

|

|

Plaintiff suing under Section 11 need only show |

Plaintiff acquired stock.

Plaintiff suffered loss.

Registration statement contained material misrepresentation or material omission . Need not prove intent to deceive or negligence or reliance on part of defendant. Only damages are remedy. Rescission not available |

|

|

Anyone who signs registration statement may |

Be liable under Section 11 |

|

|

Defendants are not liable if they can prove |

Due diligence |

|

|

Due diligence means defendant had |

Reasonable grounds to believe the facts in the registration statement were true and no material facts were omitted |

|

|

1934 Act is concerned with |

Exchanges e.g. sales, purchases of securities after issuance |

|

|

1934 Act has registration and reporting provisions that apply only |

To certain companies and anti fraud provisions that apply to all purchasers and sellers regardless of registration |

|

|

The SEC can seek suspension or revocation of company's |

Registered securities for violating 1934 act |

|

|

The 1934 act registration requirements |

Companies traded on national exchange.

Companies with more than $10M in assets and at least 2000 shareholders or 500 unaccredited shareholders. National stock exchanges, brokers and dealers must also register |

|

|

Form 10K |

Annual report filed within 60 days for large corporations (90days for small ) of the end of the year. Must contain Certified financials. |

|

|

Form 10Q |

Quarterly report filed within 40 days for large corporations (45 days for small) at end of each quarter. Must contain reviews of interim financials. |

|

|

Form 8K |

Must be filed within 4 days after major change in company |

|

|

5% or more owners must report to |

SEC, the issuer and the exchange on which stock is traded. The report must include background information about the purchaser, source of funds and purpose kn buying. |

|

|

Any party making 5% or more tender offer |

Must file SEC report |

|

|

Insiders must file a |

Report with the SEC disclosing their holdings in the reporting company and make monthly updates. |

|

|

Insiders are |

Officers, directors, more than 10% shareholders, accountants or attorneys of a company registered under 1934 act. |

|

|

1934 act limits insider trading by imposing |

Absolute liability on any insider profiting from purchase or sale in 6 month period |

|

|

Proxy solicitation |

Written request for permission to vote a shareholders shares at a shareholder meeting |

|

|

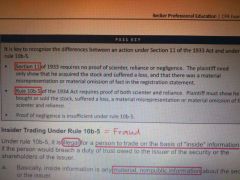

Anti fraud Rule 10B-5 applies even if |

Registration not required |

|

|

Rule Rule 10B-5 prohibits fraud in connection with |

Purchase or sale of any stock |

|

|

Violation of Rule 10B-5 can result in |

Civil damages, SEC injunction or criminal penalties. |

|

|

To recover damages for violating Rule Rule 10B-5 , plaintiff must prove |

Plaintiff bought and sold Securities. Suffered loss. Material misrepresentation or omission. |

|

|

Pass key |

|

|

|

Reselling restricted Securities under Regulation D |

Can be done as exempt from registration |

|

|

Original issue of exempt Securities sold to the public containing intentional omissions would be liable to |

Anti fraud provisions of both 1933 and 1934 Acts. |

|

|

Tombstone ad includes |

Nature of security. Price. Availability of prospectus. |

|

|

Under Regulation D, SEC must be notified within |

15 days of first sale |

|

|

Company stock listed on National exchange can make a |

Private placement offering |

|

|

Maximum time period exempt offering under Regulation D |

12 months |

|

|

CPA must use this defense against civil liability under Section 18 of 1934 Act |

Good faith |

|

|

If issuer sells security and fails disclosure requirements |

Purchaser may sell back security and get refund |

|

|

If only accredited investors invest |

No prospectus need be given |