![]()

![]()

![]()

Use LEFT and RIGHT arrow keys to navigate between flashcards;

Use UP and DOWN arrow keys to flip the card;

H to show hint;

A reads text to speech;

43 Cards in this Set

- Front

- Back

- 3rd side (hint)

|

Business services |

It is a general term that describes the work of specialised nature that supports a business but doesn't produce a tangible commodity |

Describes specialised nature but doesn't produce a tangible commodity |

|

|

Different kinds of banking services |

BITWC Banking, Insurance, Transportation, Warehousing, Communication |

BITWC |

|

|

Insurance |

Insurance facility for getting protection against risk |

Hindrance of risk |

|

|

Warehousing |

Warehousing facility for not only keeping and storing goods in a scientific and systematic manner so as to maintain their original quality, value and usefulness but also serving as logistical service providers |

|

|

|

Nature of services or characteristics of services |

5 I's Intangibility, Inconsistency, Inseparability, Inventory, Involvement |

5 I's |

|

|

Intangibility |

*The services can't be touched *Service providers work on creating a desired service as they are primarily experiential in nature. |

The services can't be touched. Therefore, the service providers need to consciously work on creating a desired service as they are primarily experiential in future

|

|

|

Inconsistency |

Services can't be standardised, like tangible products. Services have to be performed exclusively each time based on different demand and expectations of different customers |

Instead they have to be performed exclusively each time based on different demand and expectations of different customers |

|

|

Inseparability |

*Presence of the customer required. *Interaction with the process of providing services has to be managed. *Simultaneous activity of production and consumption making both of them inseperable. |

The presence of the customer is reqd. and his/her interaction with the process of providing services has to be managed. It is the simultaneous activity of production and consumption, thereby making both of them inseperable. |

|

|

Inventory |

*Services consumed at a later date can't be performed beforehand. *Some associated goods required in the process of providing services may be stored. |

Services which are to be consumed at a later date can't be performed beforehand. However, some associated goods reqd. in the process of providing services may be stored

|

|

|

Involvement |

*Participation of customer in service delivery process is must. *Customer can get services modified according to specific requirements. |

The participation of the customer in the service delivery process is must. As a result, a customer can get the services modified according to specific requirements

|

|

|

Difference between services and goods |

NT 5I's Nature, Type, Intangibility, Inseparability, Inventory, Involvement |

NT 5I's |

|

|

Banking |

*Banking facility for availability of funds to business. *Accepting deposits of money from public, repayable on demand and withdrawable by cheques or otherwise. |

Hindrance of finance to business

|

|

|

Types of banking services or commercial banks |

2B's C Bank Draft, Bank Overdraft, Cash Credits |

2B's C |

|

|

Bank Draft |

It is a cheque provided on nominal commission charges to a customer of a bank or acquired from a bank for remittance purposes, that is drawn by the bank, and drawn on another bank |

Cheque provided on nominal commission charges to a customer of a bank/ acquired from a bank for remittance purposes, that is drawn by the bank, and drawn on another bank |

|

|

Bank Overdraft |

*It occurs when money is withdrawn from a bank account and the available balance goes zero. In this situation the account is said to be 'overdrawn'. *The security for overdrafts is usually financial assets of the account holder such as shares, debentures etc. *It is a temporary facility. |

*Money withdrawn available balance zero *Security for overdrafts is financial assets *Temporary facility |

|

|

Cash credits |

*Short term cash loan to a company. *Borrower is sanctioned a credit limit upto which it may draw amounts from the bank. *Credit limit determined by bank's estimation of borrower's credit worthiness. |

It is a short term cash loan to a company. The borrower is sanctioned a credit limit upto which it may draw amounts from the bank. This credit limit is determined by the bank's estimation of the borrower's credit worthiness.Once a security for repayment has been given, the borrower company can continuously draw the specified amount from the bank

|

|

|

Types of bank accounts |

SCRFM Savings Deposit Account, Current Deposit Account, Recurring Deposit Account, Fixed Deposit Account, Multiple Option Deposit Account/Scheme |

SCRFM |

|

|

Savings Deposit Account |

*The deposits in this account are made by the persons who wish to save a little out of their incomes. *Interest is paid at nominal rate, say 4% per annum. *The rate of interest is less than that of fixed deposit account. |

*Bank account encourages small savings of households. *Deposits are made by persons who wish to save a little out of their incomes. *Rate of interest less than FD account |

|

|

Current Deposit Account |

*Most suitable for business organisation. *Depositer can deposit money any number of time and can withdrawn as and when he/she requires it. *No interest paid rather bank charge some service charges. *Money withdrawn by cheque. |

|

|

|

Recurring Deposit Account |

*Depositer deposits fixed amount of money on monthly basis for a fixed period. *Money can't be withdrawn before the expiry of that fixed term except in special circumstances. *Rate of interest on RD Account higher than SD Account. |

|

|

|

Fixed Deposits Accounts |

*Fixed deposits are time deposits wherein a fixed amount of money is deposited with the bank for a fixed period of time at a fixed rate of interest. *Interest is paid at a higher rate than SD Account. *Amount of deposit repayable by the bank after the expiry of the fixed term. |

Fixed deposits are time deposits, wherein a fixed amount of money is deposited with the bank for a fixed period of time at a fixed rate of interest.Interest is paid at a higher rate than the Savings Deposit Account.The amount of deposits is repayable by the bank after the expiry of the fixed term. Fixed deposits are time deposits, wherein a fixed amount of money is deposited with the bank for a fixed period of time at a fixed rate of interest.Interest is paid at a higher rate than the Savings Deposit Account.The amount of deposits is repayable by the bank after the expiry of the fixed term. Fixed deposits are time deposits, wherein a fixed amount of money is deposited with the bank for a fixed period of time at a fixed rate of interest.Interest is paid at a higher rate than the Savings Deposit Account.The amount of deposits is repayable by the bank after the expiry of the fixed term. Fixed deposits are time deposits, wherein a fixed amount of money is deposited with the bank for a fixed period of time at a fixed rate of interest.Interest is paid at a higher rate than the Savings Deposit Account.The amount of deposits is repayable by the bank after the expiry of the fixed term.

|

|

|

Multiple Option Discount Account |

*Combination of Savings/Current Account with Term deposit account, so that one can write cheque to the balance in MOD account or upto the drawing power available as overdraft in the current account. *Interest is paid at higher rates on the deposits. |

This account is a combination of Savings/current account with Term deposit accounts, so that one can securely write cheques up to the balance in the MOD account/ upto the drawing power available as overdraft in the current account.The interest is paid at higher rates on the deposit. |

|

|

Internet banking |

It means any user with a PC and a browser can get connected to the banks website to perform any of the virtual banking functions and avail of any of the bank's services. |

Any user with a PC and a browser can get connected to the banks website to perform any of the virtual banking functions and avail of any of the bank's services. |

|

|

E-banking |

It is electronic banking or banking using electronic media. |

*Electronic banking *Banking using electronic media |

|

|

Range of services offered by e-banking |

ATM, POS, EDI, C, E, EFT *Automated Teller Machine *Point Of Sales *Electronic Data Interchange *Credit Cards *Electronic or Digital Cash *Electronic Funds Transfer |

ATM, POS, EDI, C, E, EFT |

|

|

Benefits of e-banking to customers |

*E-banking provides 24 hrs, 365 days a year services. *Customers can make some of the permitted transactions from office or house. *It lowers transaction cost. *It inculcates a sense of financial discipline by recording each and every transaction. |

*Provides 24 hrs, 365 days a year services.

*Customers can make some of the permitted transactions from office or house. *Lowers transaction cost. *Inculcates a sense of financial discipline by recording each and every transaction. *Greater customer satisfaction by offering unlimited access to the bank. |

|

|

Benefits of e-banking to banks |

*E-banking provides competitive advantage to the bank. *Provides unlimited network. *It reduces the load on bank branches. |

*Provides competitive advantage to the bank. *Provides unlimited network.*Reduces *Reduces the load on bank branches. |

|

|

Principles of insurance |

U 2I's 2D's C *Utmost good faith *Insurable interest *Indemnity *Doctrine of 'causa proxima' *Doctrine of subrogation *Contribution |

U 2I's 2D's C |

|

|

Utmost good faith |

*A contract of insurance is a contract of uberrimae fidei. *Both the insurer and insured should display good faith towards each other in regard to the contract. *The insured must voluntarily make full, accurate disclosure of all facts, material to the risk being proposed. *The insurer must make clear all the terms in the insurance contract |

*Uberrimae fidei *Both insurer and insured should display good faith towards each other in regard to the contract. *Insured must make full, accurate disclosure of all facts, material to the risk being proposed. *Insurer must make clear all the terms in the insurance contract. |

|

|

Insurable interest |

*The insured must have an insurable interest in the subject matter of insurance. *Insurable interest means some pecuniary interest in the subject matter of the insurance contract. |

*Insured must have an insurable interest in the subject matter of insurance. *It means some pecuniary interest in the subject matter of the insurance contrac |

|

|

Indemnity |

*All insurance contracts of fire/ marine insurance are contracts of indemnity. *According to it, the insurer undertakes to put the insured in event of loss, in the same position that he occupied immediately before the happening of the event insured against. |

*According to it, the insurer undertakes to compensate (in terms of money) the insured for the loss caused to him/her due to damage/ destruction of property insured. |

|

|

Doctrine of 'causa proxima' |

According to this principle, when the loss is the result of two/more causes, the proximate cause i.e. the direct, the most dominant and most effective cause of loss should be taken into consideration. |

According to this principle, when the loss is the result of two/more causes, the proximate cause i.e. the direct, the most dominant and most effective cause of loss should be taken into consideration. |

|

|

Doctrine of subrogation |

It refers to the right of the insurer to stand in the place of the insured, after settlement of a claim, as far as the right of the insured in respect of recovery from an alternative source is involved. |

|

|

|

Contribution |

As per this principle it is the right of an insurer who has paid claim under an insurance, to call upon other liable insurers to contribute for the loss payment.

|

|

|

|

Life Insurance |

A life insurance is basically a protection against the uncertainty of life, that is death. |

a protection against the uncertainty of life. |

|

|

Main elements of life insurance |

*Life insurance contract must have all the essentials of a valid contract. *The contract of life insurance is a contract of utmost good faith. *In life insurance, the insured must have insurable interest in the life assured. |

*Life insurance contract must have all the essentials of a valid contract. *contract of utmost good faith. *the insured must have insurable interest in the life assured. |

|

|

Fire Insurance |

Fire insurance is a contract whereby the insurer, in consideration of the premium paid, undertakes to make good any loss/damage caused by a fire during a specified period upto the amount specified in the policy. A claim for loss by fire must satisfy the following two conditions:- 1) There must be actual loss 2) Fire must be accidental and non-intentional |

Fire insurance is a contract whereby the insurer, in consideration of the premium paid, undertakes to make good any loss/damage caused by a fire during a specified period upto the amount specified in the policy. *Actual loss *Accidental and non-intentional |

|

|

Main elements of fire insurance contract |

*In fire insurance, the insured must have insurable interest in the subject matter of the insurance. *Similar to the life insurance contract, the contract of fire insurance is a contract of utmost good faith i.e. uberrimae fidei. *The contract of fire insurance is a contract of strict indemnity. |

*Insured must have insurable interest *Uberrimae fidei *Strict indemnity |

|

|

Marine Insurance |

*Marine insurance contract is an agreement whereby the insurer undertakes to indemnify the insured in the manner and to the extent thereby agreed against marine losses. *Marine insurance provides protection against loss by marine perils or perils of the sea. There are 3 things involved:- ship/hull, cargo/goods and freight |

*the insurer undertakes to indemnify the insured in the manner and to the extent thereby agreed against marine losses. *provides protection against loss by marine perils or perils of the sea. |

|

|

Main elements of a marine insurance |

*Unlike life insurance, the contract of marine insurance is a contract of indemnity. *Similar to life and fire insurance, the contract of marine insurance is a contract of utmost good faith. *Insurable interest must exist at the time of loss. |

*Contract of indemnity *Contract of utmost good faith *Insurable interest must exist at the time of loss. |

|

|

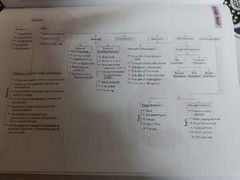

MIND MAP |

Business Services... |

|

|

|

MCQs |

Ncert MCQs |

|

|

|

Services |

Services are the acts that provide satisfaction of wants and are not essentially related to the sale of product or another services |

|